But after 1935, Florida took off and grew like crazy. Even if you bought at the peak of the bubble, by the 1940s you had still gained some value.

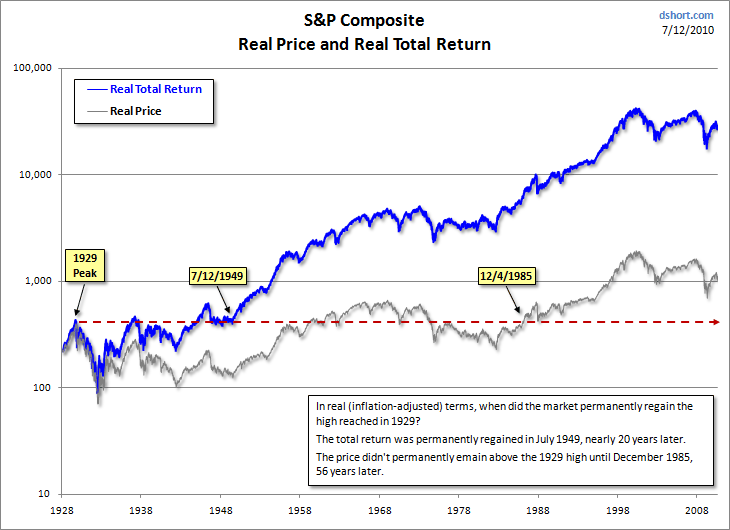

The USA stock market went through one of histories greatest bubbles from 1927 to 1929. Afterwards, it took the stock market 24 years to recover. But by the mid 1950s, the stock market was rising to new heights.

The DotCom boom was clearly a bubble in 1999, but eventually many of the ideas became far more valuable than the heights of 2000.

If the bubbles form because investors are looking too far forward into the future, eventually the future does arrive, and then you see a period of sustained growth. That is exactly what happened in Florida, with the bubble in the 1920s, and sustained growth beginning 15 years later, at the end of the 1930s, and lasting for several decades.

My point is, if you wait long enough, the economy will often grow beyond even stupidly famous disasters. To be sure, you can probably find better investments. Buying into the stock market in 1929 and then waiting 24 years to get back to that level is not great for growing your wealth. But given time, many assets do grow beyond even the bubbles.

You're forgetting to adjust for inflation. The 1927 bubble - adjusted for inflation - took closer to the late 1990s to get a reasonable return (when you were going into the second biggest bubble of all time). Nearly every investor would've died by then.

Adjusting for inflation using shadow stats, you'd still have lost money.

With the Florida land bubble - you're also forgetting property taxes.

>Adjusting for inflation using shadow stats, you'd still have lost money.

That's because shadow stats is a joke. If you adjust US GDP using their inflation figures, you'd find that the US economy has been on a continual decline for the past few decades.

> That's because shadow stats is a joke. If you adjust US GDP using their inflation figures, you'd find that the US economy has been on a continual decline for the past few decades.

Today families need dual incomes just to purchase a modest home and carry health insurance. How is this not a decline in standard of living from a few decades ago?

Where's our new airports? New rail transit systems? New infrastructure? Everything in this country is old and getting older.

Inflation is and always will be relative value story. Some airports are crumbling, some are newer. Today we have iPhone's, virtual doctor's appointments and no horse manure in the street.

And 40 years ago we had real doctors actually available for patients, no horse manure in the street, and no capitalist manure wired into our pockets 24/7 controlling our information flow thru a select set of international media conglomerates.

I’m skeptical that the things you don’t like about 2022 are because 1982 was strictly better. Seems much more likely that we simply have a different set of compromises and priorities, with some things better and some things worse and no easy way to untangle the complex interdependencies into sweeping linear statements like “decline”.

Who are you talking to? When did I make any statements of that nature?

I was pointing out the provided example was stupid. Smart phones are "cool" and all, but it'd be a tough sell to argue successfully that connectivity has increased societal cohesion, education, information dispersal, or any of the other virtues you might hope for.

Instead, iPhones and virtual doctor appointments are like bandaids on a societal-wide decline, where increased privatization combines with government inflation to create a caste system they disguise as capitalism. Inflation-adjusted salaries are lower than ever across the board, housing prices are skyrocketing both absolutely and as a function of salary-years, corporate control of information has reached unprecedented levels, and the "relative value story" of now vs 40 years ago makes it pretty clear it's tougher to have a good life now even if you can have fancy toys to interact with corporate-controlled data-mined ad-laced entertainment

I’m responding to the thread. Decline is mentioned a few posts up. Regardless of all the bad things you list, I would still prefer to live in 2022 than 1982 because I believe those bad things are stated hyperbolically and where there are genuine negatives they are more than compensated for by other factors. Are things perfect? No, let’s keep working on this and make 2062 even better.

> Are things perfect? No, let’s keep working on this and make 2062 even better

The naivety is almost making me feel better, but I don't think you understand what capitalism has done to our world's power structures if you think we stand a chance to change anything

Problem is that wages did not increase with economic growth. Those that benefit the most are a small minority, so yes, now both parents would need to work to achieve the same.

Originally, my plan was to earn enough to secure a house & future as a working person, and then try to join politic and change the discourse.

Now, my plan is to accept that even with a good salary securing a future at good QOL costs a lifetime, so I will try to enjoy myself and hopefully buy a home that doesn't get burnt down in the increasingly frequent and devastating forest fires of my native home.

> you'd find that the US economy has been on a continual decline for the past few decades.

That claim sounds reasonable given what I've observed happening in this country over the last few decades. Without question people seem to struggle much more to obtain the same level of lifestyle as many enjoyed decades ago.

You seem to claim that this is such an obvious falsehood that there's no more room for discussion, but I think there's much more room for discussion that you are implying.

When you say that you've observed what has happened over multiple decades, are you observing people within your own social circle and are those people from a diverse and representative background or are they from a narrow demographic? It's true that the relative economic status of white men has declined over the last few decades, but the economic status of women or men from other ethnic groups has grown significantly in that time.

And even then your premise is still largely false. The median and average economic outcome of white men has increased perfectly reasonably since the late 1970s. That includes both income and net wealth figures. The American white male is economically better off than the white male in: Britain, Sweden, Germany, France, Spain, Italy, and so on.

It's primarily the labor-heavy working-class white male (in the white male demographic) that has been brutalized by changes in the US and global economy. They have been left behind to drown in a pool of fentanyl.

> It's primarily the labor-heavy working-class white male (in the white male demographic) that has been brutalized by changes in the US and global economy. They have been left behind to drown in a pool of fentanyl.

That sounds like most people are actually more negatively affected by the economy compared to decades prior.

No, not "most". It's 30% or 40% of people. That's not "most". In particular, it's not enough to dominate the statistics.

Let me say very clearly: It's far too many people. I don't care if it's less than a majority, and I don't care if it swings the overall statistics. It's still too many people that are being economically destroyed.

I love hacker news, complaining about semantics when someone says most people are having their lives ruined with the clap back that it's only 40% is the best possible reply!

Most people merely struggle to pay rent which is fueled by insane zoning which people use as a cudgel to beat other residents up to get them to pay up insane prices for housing.

Outside of housing everything is dirt cheap nowadays.

> Based on my conversations with Williams, I think I now understand what he’s doing: he’s misinterpreting a cumulative 20-year change in the measured price level as a change in the measured annual inflation rate. And that caused him to overestimate that annual change by at least an order of magnitude.

Looking around that makes sense. Actual production shrank and almost no one can afford housing until they're middle aged. Walking down city streets the buildings that aren't boarded up and decaying only have "for lease" signs in the windows.

> and almost no one can afford housing until they're middle aged

...except that shadowstat's inflation figures outstrips even housing prices[1]. Eyeballing their chart, we've been experiencing 9% growth between 2000 and 2020, translating to a 460% increase. By comparison the housing price index has only gone up 184%

the US economy has been on a continual decline for the last few decades, it's jsut been cleverely masked.

that sounds quite reasonable to me, considering the vast decrease in material living standard in the US for the last several decades. there was an interview with someone who lived through the 70s that was saying a painter back then could afford to buy his own home, have a wife that didn't work and six kids! today, a single painter can barely afford to rent a single bedroom, let alone support a whole family and have a house.

Not just that, but our lifestyles have changed entirely. How many outfits did people own? How many cars? How often did they eat out? What kind of entertainment did they enjoy, and how often?

People could generally meet their basic needs because those were the only things they spent money on. Life was exceedingly bare-bones. Houses were small. Your life revolved around your job. You cooked all your own meals. You entertained yourself. The list goes on.

All of that said, house prices are alone just bad example. If you went somewhere with cheap land and no red tape, you could get a 70's house at 70's prices (adjusted for inflation) still.

I watched "Apollo 10 1/2" recently. It's about what life in America was like in the late 1960s.

One thing is that mom cooked all the meals. People rarely ate out. I know that was true in my family at the time. Eating out was a major, major treat. Entertainment was going out the door and joining up with the neighborhood kids. The house was tiny.

People rarely ate out because most people were single income families and there was one adult that had time for food preparation. Today prepared foods and eating out are a necessity rather then a convenience for most couples.

Food has also gotten much cheaper relative to what it was in the 1970’s. Some would argue that it has also reduced in quality.

People in the 1970’s bought different things than people do today. In the 1970’s people bought more formal clothing (e.g. suits) and formal dinnerware than people today. They bought more wrist watch’s and slide rules.

But if you add up all the plusses and minuses the two income family today has less disposable income then the single income family in the 1970’s when you exclude the cost of transportation, healthcare, childcare and housing.

It turns out one of the biggest drivers of home prices is school quality and income potential. So two cars for two jobs in a place you can find them and housing and childcare to ensure that children are safe.

Houses are larger but most of the housing stock is much older than in the 1970’s. Most of the 1970’s housing stock is still around, it isn’t like we tore it all down in the last 10 years and built new, larger housing.

The starter homes of the US Boomer generation are out of reach of the Millennials even though they are the same houses but now 50 years old.

only the newer ones are much larger. the ones built in the 60s are still the same size they've always been. the point is # of hours worked to afford a house of a given set size is higher today than it was in the 70s. same is true for cars too and they haven't improved much: i know i'm cherry picking here but look at a corrola from today, the mpg is 35mpg, the same as it was 40 to 50 years ago. the new one is heavier than ever, loaded with safety features rarely used, nullifying most of the mpg tech increases.

Having your spouse not work is a sign of poverty. It means that if they worked, they wouldn't be able to bring in enough income to pay for childcare.

It is possible that you're just so rich their income wouldn't contribute to the family, but income is always useful - otherwise neither of you would be working.

That's actually more reasonable than what you'd get if you combine their inflation figures[1] with nominal GDP[2]. Eyeballing their inflation chart (actual figures are paywalled), it looks like we've been experiencing 9% inflation since 2000. Between Q1 2000 and Q1 2020, nominal GDP per capita went up 82% (ie. 1.822x), but 9% growth for 20 year works out to be 460% growth (ie. 5.604x). In other words, the economy contracted by 67% in real terms. Maybe they realized that's too ridiculous even for conspiracy theorists, and revised their figures accordingly?

Why would you link to GDP PER CAPITA? Are you ignoring that population has grown since 2000?

GDP since 2000 went from 10.5T to 24T (2.285x). Adjusted for 3% inflation, that's a 26% increase.

Your point remains.

4% inflation would mean a 4% increase over 20 years.

5% inflation would mean a 14% DECREASE over 20 years.

6% inflation would mean a 29% DECREASE over 20 years.

7% inflation would mean a 41% DECREASE over 20 years.

8% inflation would mean a 51% DECREASE over 20 years.

The problem is - the way people experience inflation is dramatically impacted by whether they had a 30-year fixed mortgage.

If your house PRICE went up 400% since 2000 and your housing cost went DOWN 20% since 2000 - inflation would obviously seem low.

If your rent went up 400% since 2000, it obviously feels different.

67% of people are homeowners - and the Fed's measure of inflation seems largely targeted to this group of people. The true rate of inflation is almost certainly higher - but probably nowhere close to ShadowStats.

> Why would you link to GDP PER CAPITA? Are you ignoring that population has grown since 2000?

1. using country level GDP gets you a 63% drop, hardly any better

2. The argument I was making was with respect to living standards (ie. there's no way that our income/living standards dropped 67% in 20 years). In that context it makes sense to use GDP per capita rather than GDP for the entire country. If US population grew 50% over some time period, and GDP only grew 25%, that's actually bad because that means the average person is actually worse off than before.

"continual decline" is an understatement of how big the decline supposedly is. I calculated the actual decline in my other comment[1]. In short, if their figures are to be believed, the US economy contracted 67% in real terms between 2000 and 2020. That would put US GDP per capita between Guyana and Argentina. Even if you believe the "US is in decline narrative", it's hard to believe that it's been declining to the level of Guyana or Argentina.

I don't know enough to debate the numbers, but if we're making external comparisons, my first question is whether the calculations for Argentina/Guyana have been altered to match the US shadowstat alterations.

That fixes the problem of "US declining to Argentina levels", but now you have a new problem: did the world economy contract by 67% between 2000 and 2020?

It's not, but the GDP figures I was looking up was in USD, so it should be factored in.

>but I think you're oversimplifying things.

Perhaps, but can you think of a plausible model for why our GDP would have dropped 67% in real terms, but somehow our living standards haven't dipped to that of a developing south american/african country? The only explanations I can come up with are:

1. the real GDP drop doesn't exist, or at least is vastly overstated

2. every other country (or at least the worldwide average) GDP dropped by approximately the same amount, so comparatively speaking we're still in the same place relative to other countries

Living standards aren't really that low in Argentina or Chile. They're obviously much higher in the US, but we also have 10x more public debt per Capita, and 5x more private debt per Capita.

Please re-read my comment. I'm not saying that GDP has actually been declining, I'm just saying that if we take nominal GDP and deflate using shadowstats' figures, the US economy would have been contracting. That's an absurd statement, which probably means the shadowstats' inflation figures are off.

> Adjusting for inflation using shadow stats, you'd still have lost money.

Major red flag -- shadow stats is a hyperinflation fantasy. Of course it looks like you'd lose money if you think inflation is orders of magnitude higher than it actually was.

I remember vaguely a chart of total inflation-adjusted return, including dividends. Forgetting dividends leads some people to be much more pessimistic than they should.

The 1929 crash took just under 5 years to recover if adjusting for deflation and dividend yield (averaged 14% in that period). Nominal value took much longer but real value bounced back quick.

People who believe shadow stats don't know how exponential functions work. If you add 3% on top of an exponential function that new function will diverge exponentially from the original.

The evidence for shadow stats should be going up every year but we haven't seen that at all.

You can't just adjust for inflation like that because there's nowhere you can put your money and get inflation-rate returns. 1 dollar in 1920 is still 1 dollar now. The closest safe rate you can get is a savings account or CD but that is much lower than inflation.

I care about purchasing power over time. If inflation is going to mean that regardless of how I invest, tomorrow I will be able to buy less, then I would buy more today.

I know there are limits, like in 1920 I couldn't buy a 1gbps internet connection or a Moderna vaccine. But despite inflation's flaws, it is useful as part of a discount rate for measuring returns.

Goods don’t rise and fall in lockstep but standard figures aren’t bad.

In 1929 pig iron was 18.43$ per ton, it was $640-650 per tonne on March 7. Inflation calculator suggests it should be ~309$/ton which is fairly close across 92years but low. It also spiked to 1000+$/ton a few months later. https://www.usinflationcalculator.com/

Gasoline on the other hand was 0.21$/ gallon in 1929 plug into the inflation calculator and you get $3.53 much closer.

Chicken was 42¢/lb in 1929 New York same inflation number gives $7.06/pound today which is high.

What really messes things up is when goods stop representing the same thing across time. A new house in 1929 house was likely though not guaranteed to have indoor plumbing but AC was rare even though both where available back then. Of course 1929 AC was often focused on humility control not just temperature so again not apples to apples but in the other direction. Look for a comparable home base on floor space, number of bathrooms etc and housing prices are rising much slower than many charts suggest.

We all know that efficiencies have driven down the cost of many manufactured goods (like TVs) and scalable services (like ATMs and online banking)

We also all know that cost disease has driven up non-scalable services (healthcare, higher Ed, govt) and supply-constrained good/assets (price of land)

The basket is still useful for understanding whether an investment clears your hurdle :)

I am not convinced things break down that simply. Healthcare is probably the best example of something that isn’t compared Apples to Apples across time. The cost of an X-Ray, cast, and some pain killers isn’t seeing nearly the cost increase those charts suggest.

I think you make a good general point and I will agree, but it needs to be said that not every bubble will recover, for example the tulip bubble, beanie babies and so on.

Crypto, NFT .. who knows, only time will tell who was right.

The tulip bubble ended because the bubonic plague killed all the speculators and didn't even affect the spot market of tulips, so we don't even know what would happen. Worst bubble example.

There were several great, rational, trades with beanie babies as well that has nothing to do with the latecomers that hoarded them and acted surprised and delusional when they were holding the bag.

Out of all the famous bubbles, I think equities bubbles are more useful examples of irrecoverable irrational exuberance than any commodities/product bubble.

I think crypto has already proven itself. Every time it's increasing people say it's a bubble, then it retraces and they say "see!", and then it recovers and excels and they repeat. Only the delusion would disagree.

Pornhub's premium service already uses crypto and has since the credit card monopolies threw them out in 2020. I just checked - the only other way to pay is by ACH.

If porn is the bellwether, then use cases have arrived.

Bubbles don't form because investors look too far in the future, bubbles form because investing turns into speculation and people stop evaluating value at all and just have a case of FOMO. At that point most speculators are buying with intent to flip in a short time period. On top of that, bubbles often carry high leverage, so its not like you lose what you have, you lose what you have and then also go into massive debt(person buys $1m house with 50k down and it goes underwater, or person uses 10x leverage to trade options on tech companies and they tank).

Sure, the people that are able to cling on and wait it out for 2 decades might say 'this wasn't so bad after all!' but the people who lost their jobs or lost their families, went into bankruptcy, etc...well...you won't hear from those very often and if you do, you'll probably just say 'better luck next time'.

The USA stock market went through one of histories greatest bubbles from 1927 to 1929. Afterwards, it took the stock market 24 years to recover. But by the mid 1950s, the stock market was rising to new heights.

This also assumes you put no new money in the market and ignoring dividends. Buying the dip in the 30s, 40s would have cut this time to breakeven significantly. Also, we're talking a once in a 100+ year event. We may never see a repeat of a similar sized crash again in our lifetimes.

"Scientists have calculated that the chances of something so patently absurd actually existing are millions to one.

But magicians have calculated that million-to-one chances crop up nine times out of ten."

- Mort, by Terry Pratchett

Which actually plays out often, birthday-paradox style.

Poverty in the US went down in 2020. CARES act wasn't a "wealth transfer", but you can claim rich people made all the money if you quote stock market gains starting at the bottom of the crash in March.

What actually happened is Gates and Bezos lost half their wealth, but everyone's still complaining! Just get all the other rich guys to get divorced.

If it was a one in 100 years event or a one in 200 years event, it was still pretty mild as far as crises go. If your horizon is 50 years, there is a real risk that you will experience something far worse in your lifetime.

Yes, this is an important point. Just looking at a stock market index over time doesn’t reveal the full picture because most investors in a bubble don’t buy the index. That would be boring and they’d miss on the imminent gains on the hot stocks! So instead they pick.

If you picked ten stocks in 1928, many of them were bankrupt or near zero in five years. Same for dot-com stocks in 1999.

So now you have maybe 10% left of your original capital. You could go conservative, invest it in the index and wait. Assuming a 8% annual gain it’s going to take you 30 years to make back the money you lost (not accounting for inflation). Or you could continue picking stocks and maybe increase the risk level to make the 10x gain you need to get even.

The average bubble investor probably isn’t successful even over a period of decades.

> if you wait long enough, the economy will often grow beyond even stupidly famous disasters.

The only essential axiom you need for this to be true is infinite growth on a finite planet.

Unfortunately it looks, from multiple perspectives, like we are hitting the limits of growth.

There's a reasonable argument to be made that the true bubble we're in is an "industrial civilization bubble". All of that growth you're seeing can be boiled down to expending vast amounts of non-renewable energy. As we approach the environmental limits of that behavior, the trend you've observed over the past 250 years might not hold true.

"They hated PheonixPharts because he told the truth"

But while your point stands, there are some wrinkles when we're considering things on a human scale. We probably can have (for human purposes) infinite growth in PDF's, MP3s, apps and browser games... we just won't want to pay for them with the same currency that pays for scarce resources. And while exponential growth is impossible, there is more solar radiation hitting the planet every year and will be for a time span close enough to infinity for planning purposes. So steady growth might be possible indefinitely (again, for human purposes).

You have convinced me that hostile aliens exist. They won't hunt humans to extinction, no they will legally acquire the rights to earth so that they can maintain infinite economic growth.

Intergenerational projects are worth pursuing. Those projects require intergenerational value.

Going back to the moon, going to mars, making cities more livable, building Cathedrals, healing cultural trauma, making healthy families, creating better ways of life, enhancing health and lifespan, teaching and learning how the world works, figuring out consciousness, determining the secret to a good life, eliminating pain and creating ideal adventures… that is all possible with enough dedication on a long enough timescale and with enough forward thinking and endurance/adjustment.

I get that ending deprivation in the now is important, but I can’t help but feeling we’ve been sacrificing the future to a decades long hedonic treadmill to satisfy base and immediate needs rather than future oriented striving.

I fear it's inherent to our current interpretation of democracy. Individuals have very few incentives to look past their own lifetimes (and those incentives are almost entirely summed up as "their children"), which tends to downplay even projects that are only multiple decades. If it doesn't improve my life in 5-10 years why would I care one way or the other?

And if someone tries to propose something longer term, it'll get shot down by someone who says "how about not and we spend the money on partying instead" or the equivalent.

More and more I feel that we have to "sneak" long-term projects past people without them noticing.

You know, a positive interest rate implies that people would rather have something now than later. A 0% interest rate implies people value the future and present equally. A negative interest rate implies that people have more financial capital than they know what to do with which means it must be invested into capital with a long lifespan.

the reason bubbles form is because investors have no alternative (TINA - there is nothing else). In times of extremely high inflation (5% - 10%), you can't be in bonds or cash. So, this forces everyone into equities. Even at just 10% inflation, you'd loose half your cash in just 7 years.

and the CPI figures underestimate inflation by at least 2-3% with all their hedonistic adjustments. it used to be that economists would get a basket of goods to measure inflation. there's hardly any need for that anymore. Now that housing makes up 60%+ of everyone's (at least the latest generation of house buyers/renters) expenses, you just use housing as a proxy for inflation.

I find it amusing that nobody really cares about inflation and only about the artificially induced housing shortage which has nothing to do with economics and instead is all about urban planning. People used to build cities like NYC but now they refuse to do that.

> Now that housing makes up 60%+ of everyone's (at least the latest generation of house buyers/renters) expenses

Is that actually true for the median US resident? I have a really hard time believing it. I can believe it's the case in SF and some other big cities maybe.

not the median. But, the average person buying in at today's prices, is going to be pretty close to that. I saw one statistic that said 25% of millenials were living at home. and those that weren't, were spending 40% to 50% on housing. of course someone buying now, is even worse of than that 40% to 50%.

I think a better measure might be # of hours worked to afford 1 sq ft. (1970 vs 2022)

But with even a small amount of leverage, you'd be completely wiped out. With 2x leverage and a 50% drop in the asset price, you're broke: there is no "just ride it out."

The stock market is one thing, but anyone with a mortgage is leveraged to the tits, which is why real estate is so cyclical and the downturns can be so devastating.

This is partly due to survivorship bias. I bet that anyone who bought Argentinian stocks in 1927 never recovered their investment. A lot of the dotcom investments simply failed and disappeared. And I'm sure there are examples of land booms that never recovered either.

"We are all at a wonderful ball where the champagne sparkles in every glass and soft laughter falls upon the summer air. We know, by the rules, that at some moment, the Black Horseman will come shattering through the great terrace doors, wreaking vengeance and scattering the survivors. Those who leave early are saved, but the ball is so splendid no one wants to leave while there is still time, so that everyone keeps asking, ‘What time is it? What time is it?’ But none of the clocks have any hands."

I feel like the tech bubble is really just an outgrowth of an economic boom; big money rolls in, and needs a place to go. Everyone is happy to invest in dog shit as long as they can buy dog shit at $190/kilo and sell at 10 bucks more. They have to put the money somewhere. Tech companies are just a somewhere, but dog shit would be perfectly adequate, and arguably less overhead...

I just realized NFT's have even less overhead than dog shit.

Hey, the market for dog shit is growing since there's a looming fertilizer shortage due to the Russian invasion. Growth market... add in a scheme for tax breaks through city clean up initiatives, you may just have an opportunity.

You're supposed to compost any shit before using it as fertilizer. Appling poop directly to a plant is never really a good idea unless you water it down a lot.

Interesting. The grass around the cat shit in my garden always seems to grow much better than the surrounding grass. I'm assuming the cats also eat a carnivorous diet.

It all depends on the plant. Some plants, including grasses, take direct shit great. Others, not so much. It has less to do with the type of shit and more with the type of plant. Most shit is composted before use.

I feel like we should kill 2 birds with one stone: Bats and bat guano.

Guano used to be mined for gunpowder, to the point where the US annexed a few islands after the Guano Islands Act of 1856. If bat guano is usable as fertilizer, we could design some basic guano-collecting bat shelters that act like an automatic litterbox for cats.

The bats get a home, and the equivalent of a flush-toilet, while we get bats, less bugs, and plenty of batshit ideas.

"...and they shall beat their swords into ploughshares, and spears into pruning hooks; nation shall not lift up sword against nation; neither shall they learn war anymore"

> The Atomic Energy Commission (AEC) established the Plowshare Program in June 1957 to explore the peaceful uses of nuclear energy. The program took its name from the Bible (Isaiah 2:4), "they will beat their swords into plowshares."

How much will energy really cost in a world that's "fully" renewable in 10-20 years? Its not much different then all the datacenters built on the Colombia river in Washington state/Oregon so they get cheap hydro-electric power.

The question is will crypto and NFT's push us over the edge before we get to that point. Alongside the thousands of other similar things like people driving large SUV's instead of fuel efficient cars before we go fully electric.

Pretty much any collectible could be called a pyramid scheme. It doesn't really matter in the long run. Humans like these things because they attach value to them as irrational as it might be.

No one is melting down their Rolex for base metals. Lol. Yet they can be an extremely sound investment.

Collectibles are never 'an extremely sound investment'. They sometimes are a lucky investment.

There is no way to determine what collectibles are worth 'investing' in, they generate no cash flow, and they have a large carrying cost. Further, the market for purchase is extremely small; even if you manage to luck out in collecting something that appreciates in value, finding an actual buyer is itself hit or miss.

Even with Rolexes, which you call out, every article I've seen talks about -specific models- of Rolex. Not all of them. And the reason for that is the scarcity; if you happen to buy a sufficiently rare model, that is sufficiently iconic when you want to sell, yeah, it'll be worth more, and provided you can find a buyer (the scarcity compared with demand likely means you can, but the market is inefficient; there is no obvious safe place to sell the watch that will get bids from any and all interested parties, unless it's so high value as to warrant a well known auction house) you can liquidate it at a higher value. But that's a lot of ifs.

I never said all collectables were an extremely sound investments, just Rolex. I agree not all Rolex watches either, obviously some due diligence would need to be performed.

But yes, scarcity is precisely it. That is what NFTs are trying to bring to digital assets. Whether it will succeed or not is an outstanding question but I wouldn't straight up dismiss it altogether. Especially considering the sheer amount that has been spent on digital goods in video games which you would say have precisely zero value. Don't get me wrong, the space will be filled with scams just like real world collectables are (late night infomercials for coin collections right?)

"Due diligence" - except you can't. Did people in the 1950s know that Submariner watches were going to be a big gain? No. People bought them to wear. Why did Rolex watches persist and gain value, while Bulova watches did not? We can come up with reasons -now-, but in the 1950s you wouldn't know.

Just like with the NFT of the first tweet, 'due diligence' for collectibles is just speculation because there is nothing to base it on. Most investments have cash flow of some sort you can evaluate. Not collectibles. The expected value of every collectible trends negative, since it's a physical thing subject to wear and tear, and most physical things depreciate.

NFTs are worse than collectibles in that the scarcity isn't even of the thing; it's just an artificially created scarcity around "ownership" of an infinite thing. Unprovable ownership, no less.

If you 'invest' in a Rolex, at the end of the day you have a nice watch. If you 'invest' in an NFT, at the end of the day you have a freely available graphic.

In terms of digital goods in video games...yeah; companies have been selling digital goods for their games without NFTs for years. Not sure what NFTs are bringing there.

> Pretty much any collectible could be called a pyramid scheme.

Collecting physical items is different than NFTs even if you want to collect things just to resell them. With an NFT you've just got a database entry saying you "own" a thing. You don't have any exclusive rights to it. If anyone else can view it they can save a copy and happily enjoy it forever.

With a physical item you have possession of it and exclusive control over access to it. If you let me see it I can't make a copy of it to keep for myself. Even if you don't melt it down for its raw materials it retains some value due to just being a physical artifact that can be experienced.

The blockchain entry is meaningless. There's no canonical blockchain. There's no enforcement around blockchain entries. It's got the same real world validity as a text file on your desktop that says you "own" the Mona Lisa.

Even if someone did, I'd be super curious as to the actual return. The highest priced card sold at auction for a "you could just find it in a random pack of Pokemon cards" I could find was around $20k; all the higher priced ones were either due to printing errors (so -extremely- limited runs that you were unlikely to actually get ahold of just buying cards), or were special runs for special events (so also not something you could just buy).

Given that, the decades now that Pokemon cards have been sold, the implications buy in would have (i.e., if you went all in on Pokemon cards as soon as they hit the market, you presumably are going all in on every big IP CCG as a potential investment path, or just as liable to pick losers as winners. Those Star Trek CCG cards haven't exactly held their worth), I'm pretty sure you're not coming out ahead even if you did.

The closest analog I could come up with something like a baseball card with an authenticated signature of the player. Yes you could copy the baseball card, and even the signature, but I have the original, and it's been authenticated by by a third party expert.

In this case, the card is an image file and the third party is math (the smart contract that issued the token).

Sentimental value is based on sentiment, so you probably shouldn't try to apply objective logic to something that is subjective to every person and expect useful results.

> In this case, the card is an image file and the third party is math (the smart contract that issued the token).

There's no canonical block chain. So the same image can be resold on any number of blockchains and every buyer can claim to be the "owner" with the same legitimacy. Which is zero legitimacy. There's not even a meaningful way to verify the person selling an NFT had any rights to do so.

With a signed baseball card if you have physical possession of it then you're the owner. You have exclusive control over access to the card. Even if the card's inflated value drops because no one is willing to buy it, you still have a physical card to enjoy.

Sure there is. Anytime someone says "NFT", they are almost certainly referring to an ERC-721/777[1] token on Ethereum. What other blockchains support NFTs and have any kind of use?

Re legitimacy: how do you prove that any piece of artwork for sale in the real world is legit (the seller isn't violating someone's copyright or selling something stolen)? With an NFT at least, there's no such thing as a fake bored ape; the contract address that defined those is known. You can copy the image, you can even mint it, but it will be a trivially differentiable from the original, since it will belong to a different contract.

It's more of you own a receipt issued by a certain authority that backs your claim to the collectible item but not the item itself.

As with regards to sentimental value, I'm actually in favor of the concept in this context of collectible trading but I hardly see any application in the NFT world like for example yesterday someone posted an article about an NFT built atop Dorsey's debut tweet on the platform that plummeted a whooping 99% in value and the investor lost around $3 mln on his trade, that made me think what sentimental value could this tweet for him to warrant such a ridiculous valuation but I couldn't find an answer except it was just a vehicle of speculation for him, a very risky and foolish one in the end.

Rolex has a powerful brand for how many decades now? Not gonna Google it but probably at least 40 years. The chance people will suddenly decide Rolex sucks is very low. NFTs have a few decades to go I think before we can compare them to Rolex.

What about Supreme? or Stone Island? or Common Projects? These brands have value because of the current culture. And they will not have much value once that culture shifts.

People will spend money on status symbols and will continue to for a long time. NFT's (or something else like them) in a world with metaverses will likely become status symbols. Doesn't mean any individual aesthetic NFT has value but the general concept could survive and mirror the trends seen in (expensive) clothing brands.

And the majority of people won't care and will think it's a complete waste of money.

Well you made me Google it Rolex was founded in 1905, that is quite a few culture shifts coming and going...we can safely call it durable.

It's very possible NFTs will be the same we just don't know yet.

Yeah, but you can't generally re-sell a Rolex watch for a profit. There are some particular models for which you can, and probably a very old still-working watch will always have some kind of collectible value, but otherwise Rolexes are not really a collectible market.

I'm saying a double digit chunk of these companies' expenses and IP production is yielding no economic value: either through lack of product market fit or getting cancelled before they launch.

These companies are dripping with untrimmed fat and lack of focus on serving customers via building dumb projects that never get used.

> In particular dog-shit has more intrinsic value than NFTs.

That’s a kind of weird thing to say.

NFTs are uniquely identifiable, self-executing code, that conveys legal ownership to the holder of the NFT. NFTs can and often do represent ownership of an asset, sometimes the asset. That in and of itself gives NFTs tremendous amount of intrinsic value as a tool that represents title of ownership and can facilitate trust-less transfer of title/ownership. I think you are right NFTs in their current use case are most often, but not entirely, used to represent ownership of classes of assets that are meant to be transferred/sold, but intrinsically NFTs still value as a tool that can represent ownership of a give asset.

In other words one might say dog-shit has more intrinsic value than a written contract, except that contracts can and often do create enforceable terms (though not always) thus giving contracts intrinsic value, as evidenced by contracts being one of the most successful tools in all of human history as part of the historic record as far back as the written record goes.

> NFTs are uniquely identifiable, self-executing code, that conveys legal ownership to the holder of the NFT.

> NFTs can and often do represent ownership of an asset, sometimes the asset.

> That in and of itself gives NFTs tremendous amount of intrinsic value as a tool that represents title of ownership and can facilitate trust-less transfer of title/ownership.

That is a lot of word salad.

Does an NFT confer ownership to any real, personal or intellectual property as understood by any currently existing legal authority?

My understanding is that the answer to that question is "No", invariably presented as "No, but..."

Yes. NFTs can convey ownership of real, personal and/or IP.

For example, take Bored Apes Yacht Club NFTs. If you own a BAYC NFT, then you receive commercial IP rights to an underlying image.

Assuming we both reside somewhere in the US, if I were to begin commercially producing products bearing your image, then you individually (as opposed to Larva Labs the company that created the copyrighted image) could sue me for injunctive relief and damages.

Alternatively, if someone were to mug you and force you to open your phone and transfer your BAYC NFT to their wallet, it would most likely be considered grand theft because the dollar amount of the property involved. Further, you would also have a remedy in civil law to sue the criminal for the damages. It’s not treated any differently that any other property theft.

And of course if you buy the BAYC NFT and later sell it for a profit, the IRS treats it as a capital gain and you have to pay taxes subject to penalties and enforcement action.

From the legal perspective most recently Wyoming passed a law creating and establishing the first DAO LLC legal entity, which is a LLC that can be algorithmically managed by smart contracts/holders of NFTs. This further formalizes legal recognition under the law.

>>"Does an NFT confer ownership to any real, personal or intellectual property as understood by any currently existing legal authority?"

Conceivably you could use it the same way you'd use a ticket to be redeemed for a later good or service which would presumably be recognized by existing legal authority.

I haven't heard of any actual NFTs that granted any powers that your average pog doesn't though.

> I haven't heard of any actual NFTs that granted any powers that your average pog doesn't though.

Not sure how familiar you are with the NFT space, in another comment I used Bored Ape Yacht Club as an example, let’s start with that.

If you own a pog, does that give you commercial rights to monetize the copyrighted artwork on the pog? Admittedly I’m not overly familiar with the pog market, but I don’t think purchase of any pog gives the own any underlying commercial rights to the IP.

It’s true not every NFT/NFT collection bestows the owner with commercial rights to a copyrighted work, but Bored Ape Yacht Club NFTs is just one example which provides owners commercial rights to the underlying copyrighted image.

More importantly copyrighted works, like artwork, are not the only assets an NFT can represent. Further, you are correct with your example that they can be, and in fact have been, used to represent the right to redeem for a specific good/service by any bearer. Ticketing is in fact one such real world example.

I can make you a pog that does that, yeah. It's just a matter of writing it on the pog.

I can make you a pog that bans you from a club while you hold it too, for the bored apes example. Generally a bouncer will remember you when you come back the next day without the log though, which is a slightly better ban than NFTs can handle

What I can't do is make a pog that burns your house down when you try to sell it or give it away. That's a feature unique to NFTs afaik

You attach to the pog the same meaning in the same way. Non-fungible tokens by design solve the problem around "how do I trust that this is the correct token", but thats only a problem you need to solve in low trust environments.

> Non-fungible tokens by design solve the problem around "how do I trust that this is the correct token"

I don’t agree that is the only problem they solve, but assuming arguendo all an NFT did was solve the problem of trust, then that alone makes them more intrinsically valuable than dog shit. I mean I think HN has really lost the forest for the trees when it comes to NFTs.

They don't solve "the problem of trust" but instead the much narrower "how can a group of entities, who mutually do not trust each other, have a ledger whose state they can all agree on". Crypto loosely solves trust in trustless environments, but I'm having a hard time finding where that is nicely applicable. Most transactions already require a certain base level of trust. So, yeah, dog shit has a pretty clear use case and value whereas NFTs do not. Would love counter-examples for that though. The best I've found is in the art world, where having a token that corresponds to a given work would make it much easier to track the "official" version (vastly reducing the value of any more than one forgery substantially), and I guess the various traders and dealers don't have a high degree of trust in one another so this public and distributed ledger would help with that. Obviously a lot of other problems but it at least demonstrates a hint of some value.

> Does an NFT confer ownership to any real, personal or intellectual property as understood by any currently existing legal authority?

I can use my imagination and predict a future where some form of the tech can be. But on a different note, traditional art doesn't need to be understood by any existing legal authority and people collect art. Although a lot of high value art is also used for money laundering. I just don't see a huge difference between the two in the creative category and at least NFTs have some interesting tech to them.

> traditional art doesn't need to be understood by any existing legal authority and people collect art

The content of the artwork is immaterial. Physical possession and real ownership are very well legal concepts and well covered by the corpus of laws essentially everywhere. There's even international laws covering possession of physical things.

Sure NFTs can be a useful tool, but they are more of an 'idea' than an object at that point so it gets hard to assign a value to them.

Indeed the whole problem here is that we're trying to assign intrinsic value to something which isn't fungible in the first place (which makes the notion of a market for them somewhat problematic).

So yeah I'm going to maintain that NFTs are, by design, all extrinsic value. And if someone is offering free NFTs or free dog shit you're more likely to get some use out of the latter.

> And if someone is offering free NFTs or free dog shit you're more likely to get some use out of the latter.

I only own 1 NFT that was free to mint (NFT Worlds) and the floor value is ~$20k, plus they airdropped some tokens worth over $5k. It also just so happens this is one of the NFTs someone will get more use out of than dog shit.

Market value aside, the intrinsic value of the NFT is that at any moment I can trustlessly make it available for acquisition and the prospective buyer doesn’t need to worry that it’s a counterfeit, and I don’t need to worry about any chargeback. However, you are correct that depending on the asset a given NFT represents, there could be additional real world components rendering the NFT to something of legal title to a real world asset, but the intrinsic value of the NFT remains (the ability to trustlessly sell/acquire legal title in a censorship resistant global market).

You should consider the opposite. Keeping interest rates artificially high by borrowing ever more money.

I don't know where people get this idea that reducing demand for borrowing and increasing savings is supposed to raise the interest rate. Borrowing more money increases the demand for capital and thereby the interest rate.

If the government didn't have to borrow a dollar for every dollar that was taken out of circulation the interest rate would be negative and people would be discouraged from saving more than others want to be in debt.

It goes even further than that, rates are low for about 40 years now. Yes they are super low now at around 0% , but when/if they go back up to 4-5% that is still historically low.

> I feel like the tech bubble is really just an outgrowth of an economic boom; big money rolls in, and needs a place to go

This is true, but missing an important aspect: This is what happens when you have an economic boom that primarily goes to the already-wealthy.

When there's an economic boom that goes proportionally (or more) to the middle-class and below, there's no need to figure out where the money should go. It goes to fixing up the house, to paying down debts, to paying rent, to buying new clothes.

The only time money "needs a place to go" is when it's coming in to people who already have more than they know what to do with.

But capitalism is all about wealth concentration. Giving more to those who don't need it is the entire point because that excess capital can be used to run an economic siege. Just wait until your enemy runs out of capital.

Decentralizing wealth and giving employment opportunities to those who actually need them is more of a Rootbug/Freiwirtschaft thing.

Sure would be nice if we parked all the new money in beneficial social programs instead of billionaires’ accounts just aiming for their new high score.

Except that thesis is just wrong when your mother uses Facebook, Google, Amazon, Apple, Uber, and the kids pay for Netflix (oh shit, your mother too), and their bosses buy SaaS apps for the team.

Yeah, it’s not a place to “park” money. That idea at this point sounds like conspiracy theory stuff.

I still don't, I'm afraid. I don't know which "point" you mean, having listed several, and I don't know what "take the trial into semantics" means.

I'm not sure why you rant at someone trying to understand you, and why you'd choose such vague, rhetoric-heavy wordings if you would like people to comprehend you.

Goes to show how useless these forecasts of 'bubble', 'crisis', 'froth', etc. are. Home prices in the Bay Area still going nuts despite endless predictions from 2013-2020 of bubble.

If prices are rising 20%/year then all you need are 3 years of gains to come out ahead even if the bubble bursts. Each year that passes in which prices rise and the bubble does not burst means you're one year closer to crossing the point at which even if the bubble does burst you will not lose money.

Waiting for the bubble to burst, whether it's stocks or homes, often means missing out as prices keep going up year after year. Even if the market does crash, you will never get a chance to buy back at the price your originally wanted to buy at. If you didn't buy a home in 2013-2017 because of bubble fears, even if the market does crash, you will not be able to buy at those prices again. To quote the Superbowl FTX ad, you did miss out.

There is a great Jewish joke about markets: Shlomo was returning from Antwerp, when he met Moishe: "Look at this bag of diamonds I've bought there! only 1000 florins, it's easily worth double that!"

"Wow, that's a hell of a bargain, how much do you want for it? 2000?" "deal!".

Shlomo went home. He told his wife Sarah about his daily business. "So Moishe bought this bag for double the price without bargaining? He must know it's worth much more than that, you moron! Buy it back tomorrow!"

The next day, Shlomo met Moishe : "listen, I'll take back the bag of diamonds. 3000 florins?" "deal!"

That night, Moishe told the story to his wife Debrah. "Imbecile! can't you see you've been gamed? You're now 1000 florins poorer than yesterday, and what do you have?"

The next day, Moishe met Shlomo: "listen, I've think about it, I want to buy back the diamonds. 4000?" "deal!"

So this little back and forth game goes on for a week, when someday, Shlomo said to Moishe: "Listen, I'd like to buy the diamonds back after all..."

"Too late, I've sold the bag yesterday to a merchant from Hamburg!"

"What? You've sold a stranger a bag of diamonds that was making us 1000 florins A DAY?"

This is what is called a "ladder attack" in the stock market.

Essentially you and a small group of people pick a low volume penny stock, and trade it back and forth amongst yourselves for more and more money each trade. Then other people see the fast rise and want to get in on the action. Volume picks up and the original traders cash out at a much higher price.

Tons of tech stocks and valuations, especially the unprofitable ones, are down 50-66%. It definitely burst. Supply shortages, inflation, and the war provided a sanity check.

On the other hand, 2021 was the biggest venture year ever. Everyone made a ton of money in the stock market, and needed to do something with it. The returns on ventures mean that its now a real investment channel that is here to stay.

Absolutely, where is this narrative about the bubble not bursting, and cheap money this, and market irrationality that coming from? It totally did burst. Growth stock got killed early this year across the board. The market has punished Covid hype investments (e.g. Peloton, Zoom) very hard as well.

People are very bad at predicting true change in the fundamentals of how they live their lives and then dealing with the implications of that. We've been lulled into the myth of a steady-state economy by the post-WW2 Pax Americana. If that's your model, any rapid change is a "bubble" that's going to pop and return us to our original steady state, and real lasting change is consistently undervalued.

Here's a pop quiz with a counterintuitive answer: if Bitcoin succeeds at replacing the dollar as both the world reserve currency and the currency of choice for everyday transactions, what's its fair market value? Most optimists would divide total dollar supply ($21T) by total Bitcoin supply ($21M) and come out with $1M. But the true answer is infinite: if this scenario actually comes to pass, the dollar's value will trend to zero and the question will become meaningless, as you won't be able to trade your dollars for Bitcoin at any price.

So it is with tech: software is actively replacing many core industries, which sends their value to zero and the owners of their software replacements to effectively infinity.

I suspect similar dynamics are at play with prices in general and particularly asset & housing prices. Everybody's calling a bubble and thinking they'll buy stuff later when prices come down. That can happen in localized instances (like lumber last summer), but oftentimes those bubble bursts reverse themselves and end up driving higher. Lumber went up by 250% again in the second half of last year, just as tech company stocks have reached heights that were unimaginable in the dot-com boom. The overall price level in the economy isn't going down.

> Here's a pop quiz with a counterintuitive answer: if Bitcoin succeeds at replacing the dollar as both the world reserve currency and the currency of choice for everyday transactions, what's its fair market value? Most optimists would divide total dollar supply ($21T) by total Bitcoin supply ($21M) and come out with $1M. But the true answer is infinite: if this scenario actually comes to pass, the dollar's value will trend to zero and the question will become meaningless, as you won't be able to trade your dollars for Bitcoin at any price.

That makes no sense. Assuming dollars remain legal tender (note that those words that actually mean something specific and are not synonyms for currency) in the United States, they will always be worth something. Further the fact that there are dozens of currencies in the world which are not typically reserve currencies, but are also not worth zero indicates a gap in your analysis.

This hypothetical assumes dollars do not remain legal tender - at least in the sense that people would not be willing to offer credit denominated in dollars.

Currencies have pretty strong network effects - there's a strong incentive to use the one most widely accepted, because you can then spend it in the most places, assuming free trade and common markets. That's why national currencies like the deutschhmark and lira have largely been replaced by the euro. Or, for that matter, why BCH, BSV, and ETC are virtually worthless while Bitcoin and Ethereum's value has skyrocketed.

> what's its fair market value? Most optimists would divide total dollar supply ($21T) by total Bitcoin supply ($21M) and come out with $1M. But the true answer is infinite: if this scenario actually comes to pass, the dollar's value will trend to zero and the question will become meaningless, as you won't be able to trade your dollars for Bitcoin at any price.

This isn’t valid. You’ve said the question would be meaningless and then use its answer. There’s a shell game here. You’re saying we can measure value in dollars, then we can’t, therefore anything measured in dollars truly has infinite value. I think this is obviously not true. In this scenario, the value of my hat would also be infinite.

In a sense, most of the so called bubbles occurring right now are due to a lack of tech and innovation. The issue isn’t that Home prices are inflated, the issue is our most innovative solution for home ownership is credit hand outs. The Finance sector is not innovative enough to solve this. We’d need to think about building denser cities and pragmatic modern housing. Affordable housing doesn’t have to mean “middle or low income in certain area”. These are old industries of finance and old progressive ideas that simply are not disruptive enough.

>the issue is our most innovative solution for home ownership is credit hand outs

I'm fairly certain we have more innovative solutions, but the risks just aren't lucrative for the far majority of investors. It's a lack of (relatively frictionless) experimentation more than anything.

The majority of solutions I imagine directly contrast typical western individualism, too.

The problem with housing is not technical - it's the people want their house to go up in value as much as possible. The easiest way to accomplish that is to limit supply as much as possible.

If you already have a housing shortage and >67% of the country hell-bent on making the shortage worse - technology is not going to solve the problem.

It feels like a lot of money, but I'd point out that even venture's blockbuster 2021 year, where it raised ~$128B in funding, is still far less money than Apple's ~$202B and Google's ~$169B cash on hand. Those are single companies.

The heterodox truth is that startups are undervalued for their value potential. When single (venture backed) companies all have more cash than the entire ecosystem on their balance sheet, it becomes clear that the market is undervalued.

Markets have become disconnected from reality. Maybe that's not entirely a bad thing. But it's the death blow to the ideas that markets can be a foundational organizing principle of society for the sake of allocating scarce resources. The market will remain irrational longer than society can remain solvent.

That's not to say that there isn't a role for markets, but it's apparent that they need ongoing heavy-handed intervention to keep their incentives aligned.

Inflation is near 10%. Fed funds rate is 0.5%. The govt is handing stacks of cash to people. M2 growth peaked last year at 25%.

I wonder why the bubble never burst...a real puzzler, probably a question that scientists will never work out (btw, this sarcasm is real, you have people at the Fed who think like this, this is why inequality has skyrocketed...even relative to 2010, when inequality was already high, we are up multiples...no-one has really examined this thoroughly, the Fed lacks the ability to think proactively, it is always reactive/backwards-looking).

Something that perpetually puzzles people who don't work in finance (and even then, most people in finance never get it)...because something will happen eventually, it does not mean it will happen today.

There is this pervasive mindset: if the value of X is Y, then it should be Y today...or else, why would anyone buy it at Y+10. In finance, the day of reckoning can be postponed for a very long time. Borrow more, make the interest payments, hope something changes. You see this with companies: they don't go bust until someone asks for their money back.

And people do not have expectations that separable from today's prices (thankfully, economists are now integrating this into their understanding of inflation)...if something is trading at X, people think that is the same thing as it's value rather than a function of supply and demand in the short-term. To make this conclusion more explicit: the value of a company it's future cash flows, you can say your company is worth $1bn, $10bn, $100bn...but at some point that money has to convert into cash, that is what value is.

(The gap between now and "then" is how you make money investing. It is very easy to tell what is going to happen eventually, you can make money because most investors are unable to psychologically bridge that gap, they need today and now. Unf, policymakers have exactly the same mindset...someone else's problem, tomorrow, tomorrow, never today).

We aren't in the early 2000s anymore. Tech companies won't be seen as a "fad" any time soon. As long as VCs keep making money out of diversifying risk, the "bubble" will never burst.

Early 2010s tech boom, while it involved a lot of money, felt like it was directing money at generally useful things. Cloud, Big Data, AI etc. were “buzzwords” but were generating real value for companies that used them correctly. It seemed like VCS had learned from 2000s.

With web3 we see a lot of vaporware and pyramid schemes. It is unlikely to pop like it did back then considering how entrenched technology is today but it would still wipe out a lot of value and further entrench the bigger companies.

Societal and cultural understandings of what "tech" is has shifted dramatically in the last 20 years. Home computers were still pretty niche, constant connectivity via pocket size computers was a work of science fiction, and we didn't have an omnipresent internet retailer that could bring you nearly anything in a few hours/a couple days.

The possibilities of the internet and tech companies were still in their formulative stage with regards to the general population. It's now so engrained in our daily lives that it's taken for granted.

I suspect the bubbles that will actually burst are going to be incredible niche. Even then, things like NFTs may survive due to a cultural imagination that allows ideas to live on longer than maybe they should.

I remember two partners from Andreessen Horowitz gave a presentation to a group of investors and journalists around 2015, where they had a slide with literally the title "This time is different".

I thought to myself this will not end well, major crash around the corner. I am annoyed that they were right.

I mean, every time is different in the sorts of companies/sector of the economy that fails. The large tech companies actually do have solid fundamentals. The dynamics of the business cycle remains the same though and some more speculative companies will fail (taking a look at the 6-month performance of Asana, Palantir, Zoom, etc makes me quite happy as a shorter).

Was thinking that last night too. It would also be dumb of the US to allow tech to take a big hit considering it would prevent us from competing with other countries at all levels.

This isn't very helpful, as most of the article isn't readable without the JS that the NYT serves. Also, it seems like this article _isn't_ behind their paywall.

Yes this is an odd one. This thread led me to view the original, and I was not paywalled, and all was good. But then I shared it with friends because it wasn't paywalled... and they were paywalled.

I mean there were some blow ups. WeWork, Theranos, etc... But the era of cheap/free money is just starting to end, so I think the bubble is still ahead of us.

> But the era of cheap/free money is just starting to end

Don't think so, there's an absurd amount of money in the world, mostly owned by a few rich people, and rich people aren't just going to let it sit idle without trying to invest it in something.

> Maybe somebody will invent a new kind of real estate or biotech will explode.

Which would require tech behind the curtains in order to innovate (I would dare to say that any real state or biotech company would need a "high" amount of "good" tech in order to disrupt the market... so these companies would, in essence, become tech companies).

Interest rates for bonds are starting to rise, and will need to rise a lot more to fight inflation. They are walking a fine line between high inflation and killing off companies and governments that have grown dependent on super low interest rates.

I'm not sure I understand this. Isn't web3 mostly just the use of decentralized systems?

You don't need crypto for that. If your answer is incentive, I'm not so sure you need that either.

For example, if you want to store something on the web, why not rely on a automated torrent protocol deamon in the browser that caches and seeds any datasets that you download? That solves a problem without crypto.

I think they use crypto for monetization, whereas current or “web 2” mostly uses ads as the solution to monetization for a lot of web stuff.

Eg. Sia File Transfer is a Technology for (Decentralized) File Sharing, while Sia Coin is the monetization side. Same as Helium Network, which is a LoRa Router whereas you get paid in Helium Tokens

> Isn't web3 mostly just the use of decentralized systems? You don't need crypto for that.

Maybe you do need crypto for that. One of the properties of large, decentralised systems with high stakes things running on them is that they are larger than any group of entities that can trust each other with such high stakes, so they need a mechanism to hold it together. Right now that mechanism looks like crypto of one sort or another.

Perhaps I was loose with my language. Most things need crypto - but they probably don't need cryptocurrency. Or really any currency at all. What's wrong with hosting a server from your house? What's wrong with torrent? These are decentralized and don't need crypto currency.

> What's wrong with hosting a server from your house?

Nothing, but if you're hosting just your own site, that's not what people mean by decentralised.

If you're part of a swarm all hosting replicas of the same data or providing replicas of the same service, that's decentralised, but if you're operating a large server, you're highly incentivised to be selective which data you host, to save on costs among other things. The result of many people doing that is what we see with torrents.

> What's wrong with torrent?

Torrents are a great example of when cryptocurrency tokens can improve decentralisation.

Torrents are notoriously unreliable. If you want a specific file, it's sometimes available, sometimes not, depending on the file's popularity. For things which are less popular, it's down to luck whether someone else is seeding at the moment. You may even download half of a large file, only to find the seeder takes themselves offline and you can't get the other half for weeks, or ever.

When you depend on one or two seeders for a particular file, that's not decentralised. You can't build serious infrastructure on something that unreliable.

Some cryptocurrency tokens are designed to change this. Through something called proof of data availability and cryptocurrency tokens specially designed to link to those proofs, they set up a balance of forces called cryptoeconomic incentive which ensures a lot more people are motivated to continuously make a large amount of torrent-like data available as a service, and it's hard to cheat that system.

People don't waste bandwidth uploading the contents that nobody is currently requesting, but they are effectively paid a small amount to store data and keep it ready to upload, so the incentives promote continuous high-availability of large archives of data, including unpopular and obscure files that people struggle to find and download from ordinary torrent services.

Every economy has boom and bust cycles, so "the bubble is still ahead of us" is a meaningless statement since it is true by default. Yes there will be a slowdown at some point, but can anyone can predict when and how big that will be.

Why they are considered as such by many on here (alongside AirBNB to mention another name) is either a source of puzzlement, or a triumph of marketing, depending who you ask.

Good timeline, the one commonality though during the NYtimes chart is that money was cheap(low interest rates). At the start of their timeline - 2011, fed interest rates were 0 and stayed that way until 2015, they then creeped up slightly hitting a peak in 2019(2.5). Rates then went back to 0 due to the pandemic[1]. In addition trillions of dollars were created out of thin air and that contributed alot to funding during the pandemic.

What kept rates artifically low was inflation was also low, now that inflation is skyrocketing the fed has signaled that rates are also going to jump. This is really bad for growth companies and you can see for yourself by looking at stock prices on a 6 month timeline(from today) and see the huge drop in valuations($sq, $roku, $afrm, $pypl ...) I expect these valuations to tumble by the summer even further as rates increase.

Because of the war in Ukraine people in the US aren't hearing as much about what is going on with Chinese real estate these days. TLDR: There is enough vacant housing in China to house Spain. Prices are going to drop, probably.

People have been saying there was a bubble in Chinese real estate for ten or twenty years and all that time prices have been going up in ways that are probably at least sustainable based on a growing economy.

I think the biggest movements of overvaluation are like Chinese real estate where people over pay, but the underlying value is still going up so you can keep justifying overpaying for years. Probably GE was like that for a long time. Now I think Tesla has been over valued for a long time (maybe not-- just take it as an example) but it's hard to argue it is over valued because at the same time the price appreciates the value of the underlying thing is also growing.

> There is enough vacant housing in China to house Spain.

This sounds bad off-hand but you have to consider the scale of China. Spain's population is roughly 3% of China. 3% of the US population is 10 million, which is less than the 16 million vacant homes in the US (https://www.nytimes.com/2022/03/10/realestate/vacancy-rate-b...). And that's still a generous comparison since more than 1 person lives in a home.

~90% of people in China are homeowners [1]. China's investments are extremely disproportionately R/E compared to other countries (70% vs 35% for the US) [2].

The CCP has immense pressure to prop this bubble up, and they have many options:

* Lower lending standards (you need to put 25% down to buy a house in China, but only 3.5% in the US)

* Lower interest rates (mortgage rates are negative in some parts of Europe, but ~5%+ in China)

There is enough vacant housing in China to house Spain. Prices are going to drop, probably.

It’s better to look at this from China’s vantage point. Truly, enough housing to house Spain is not enough. Perhaps for Spain it is, but we’re talking about housing China - 1bn people.

As for tech, I don’t think we’re even close to saturating the globe with technology. We’re in such an infancy that we literally need something like Starlink to get everyone connected.

There is an idea floating around the econosphere that China helped build all this housing while raw materials were cheap. You will note as well that China also ended their one child policy in 2016. So it is possible that they were building houses for a population they knew they would need to house in the future.

Not every country is a as stupid as the united states.

This is so weird, I wasn't saying Chinese government was stupid. All I said was that prices may go down. I don't know how you could look at their economic progress in the last thirty years and not think they are doing something right.

And if you think the US is stupid, well I hope you don't live there.

Isn't it kind of dangerous to make these types of plans regarding humans well into the future? We're talking two to three decades of potential leeway time until a new generation from birth to workforce will occupy these homes. A lot can change in 30 years. 30 years ago China was an extremely poor country, 30 years from now it can easily go the way of Japan with births crawling to a near halt.

It's one thing to plan infrastructure (building railways, ports, and energy), but another to hopefully assume the human element will be consistent.

It reminds me of the of when Romania in the late 1970s banned abortion and contraceptives [1].

That's fair, but should the lead time for housing projects be several decades? I'd think it'd be easier to zone the potential land first and worry about building when you can anticipate demand.

"EM's cultlike fanbase" has no power to drive up the stock price in any possible way other than ultra-short-term (and even then, it would be a really large stretch). Retail investors don't have such power in general, aside from when it comes to very low volume and low cap tickers (which Tesla is neither).

There could be many potential ways of justifying why Tesla stock is overvalued (if you are inclined to believe so), but "retail is just being irrational and hypes it up, because they are superfans" is just one of the most off-base ones.

I think it's more than retail investors. I think it's the hype and noise that his followers make, plus whatever noise he himself makes.

I think he's a bit like Trump in some ways. Trump was often said to represent an image of what a certain demographic of people thought was rich and successful. He made a lot of noise, threw around a lot of money, and his followers in turn made a lot of noise.

EM(I write it as such because I'm sick of seeing the name everywhere I turn) seems to have the image of "tech guy who struck gold" and "can't stop making money". While some of his success is definitely attributable to himself, I feel like people give him too much credit and celebrity status. I think the biggest drivers of his success are a gigantic war chest of money, combined with a massive following, and enough ideas to spend the money on.